Lake Tahoe real estate starts the year off with a bang! Quarter One saw sales volume rebound from Q1 2023 lows. In all micro-regions, the number of single-family homes sold increased year over year, with growth rates ranging from 35% to 131%.

Inventory remains low, while the demand for homeownership in Tahoe remains high, despite high interest rates. Properties that are appropriately and strategically priced are moving quickly, and the buyer pool is anxiously awaiting the influx of listings we typically see each year when the snow begins to melt.

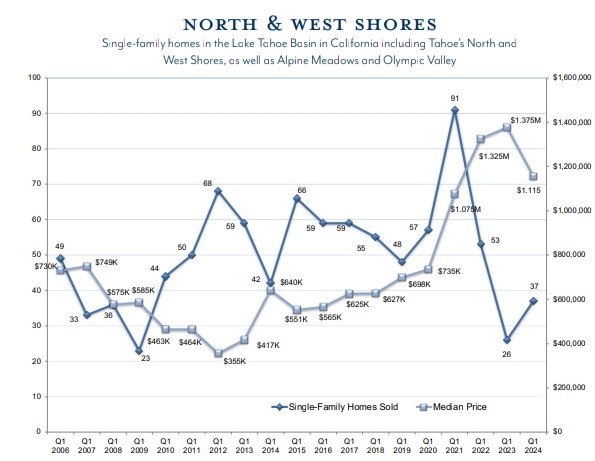

Single-family homes sold increased 42% year over year.

Median price decreased 16% year over year.

Average Days on Market was 100 days, a 43% increase from 2023.

5 of 37 homes (14%) sold for over $2 million. 1 homes (2%) sold above $5 million.

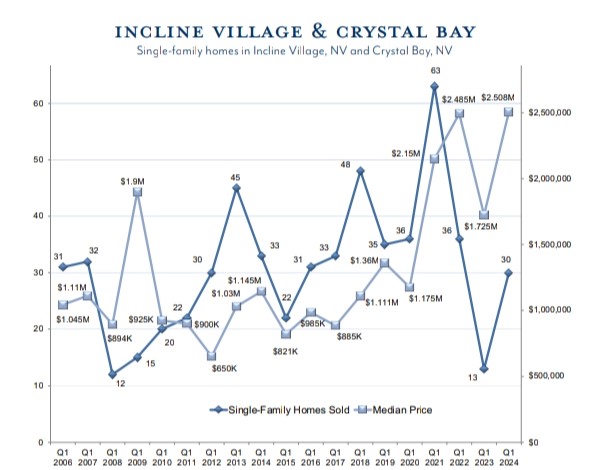

Single-family homes sold increased 131% year over year.

Median price increased 45% year over year, reaching a record high.

Average Days on Market was 140 days, up only one day over 2023.

19 of 30 homes (63%) sold for over $2 million. 4 homes (13%) sold above $5 million.

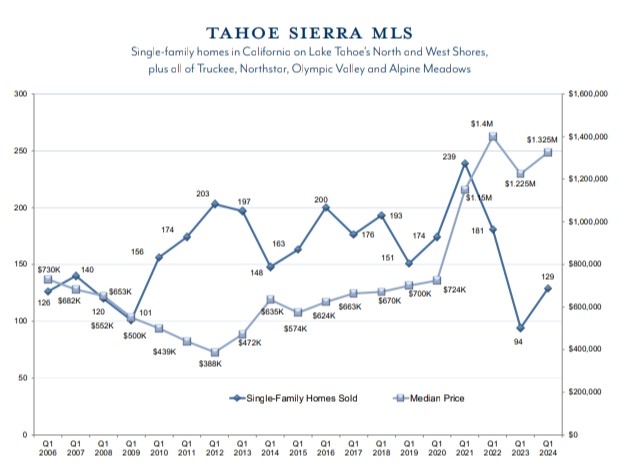

Single-family homes sold increased 37% year over year.

Median price increased 8% year over year, nearing the 2022 record high.

Average Days on Market was 75 days, a 9% increase from 2023.

32 of 129 homes (25%) sold for over $2 million. 6 homes (5%) sold above $5 million.

For more information on the Lake Tahoe real estate market, contact Amie Quirarte.

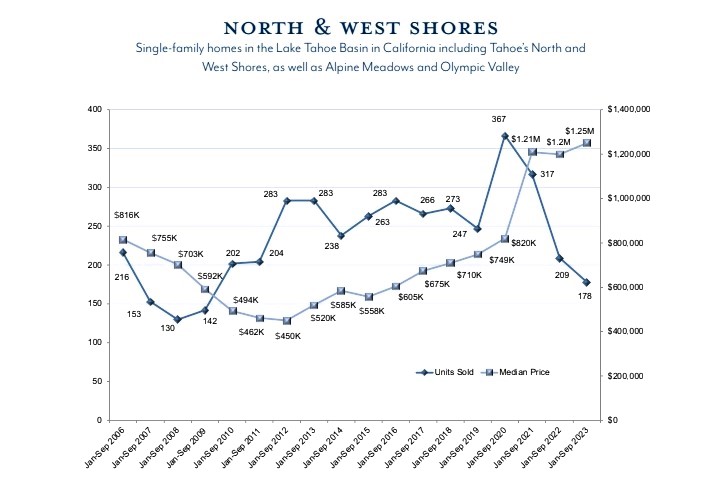

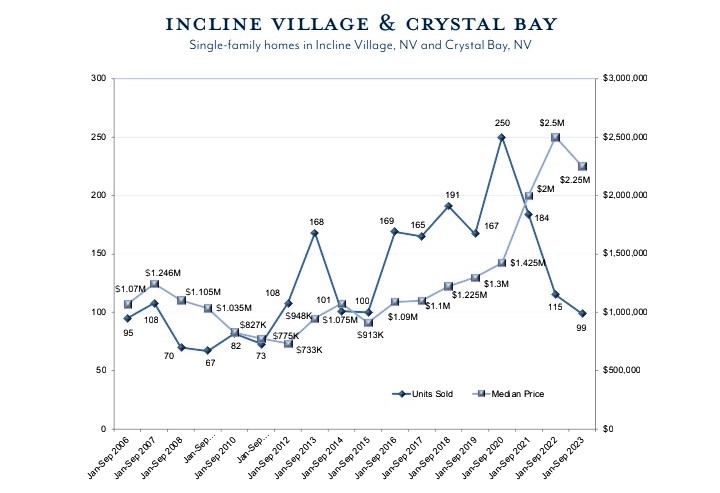

In the first three quarters of 2023, all micro-regions with the exception of lakefronts continued to show a deep decline in the number of single-family homes sold. In fact, sales volume this year has hit decade lows. Median price has been far less impacted and, in all micro-regions, sits above pricing in 2021. The supply of available homes for sale remains at about half of pre-covid levels, which at least partially explains the retention of values. With a late start to summer, after our historic winter, lakefront sales began to rebound in Q3 but still hover around the lows we saw in 2009, yet median price reached a record high. In Incline Village & Crystal Bay, 14% of single-family homes sold above $5 million.

The ongoing discrepancy between the dramatic dip in sales volume compared to the minor movement in median price reminds us that post-covid pricing may be the new normal, despite slow sales. A burst in September real estate activity balanced the sluggish start to the season and is signaling a recovery of unit sales. Now, all eyes are on Q4 as we anticipate this fall momentum will bring a strong finish to the season, equalizing Q1.

Single-family homes sold decreased 15% year over year, hitting a 14-year low.

Median price increased 4% year over year.

Average Days on Market was 44 days. In 2021, DOM was 37. In 2019, DOM was 77.

32 of 178 homes (18%) sold for over $2 million. 8 homes (4%) sold above $5 million.

Single-family homes sold decreased 14% year over year, hitting a 12-year low.

Median price decreased 10% year over year.

Average Days on Market was 119 days. In 2021, DOM was 86. In 2019, DOM was 166.

56 of 99 homes (57%) sold for over $2 million. 14 homes (14%) sold above $5 million.

Single-family homes sold decreased 25% year over year, hitting a 14-year low.

Median price decreased 4% year over year.

Average Days on Market was 44 days. In 2021, DOM was 27. In 2019, DOM was 66.

114 of 531 homes (21%) sold for over $2 million. 36 homes (7%) sold above $5 million.

For more information on the Lake Tahoe real estate market, contact Amie Quirarte.

This past week the Federal Reserve raised rates for the 10th time in a little over a year. Let’s discuss what happened as we await yet another Fed rate hike next Wednesday.

As we expected, the Federal Reserve raised the Fed Funds Rate to a range of 5.00% – 5.25%. Remember, this interest rate affects short-term loans like credit cards, autos, and home equity lines of credit.

The big question is whether this will be the last hike. When the Fed statement was released, the markets believed the Fed was signaling a pause by omitting the following line from the previous statement: “The Committee anticipates that some additional policy firming may be appropriate.”

However, shortly after the statement was released, Fed Chair Powell hosted a press conference and right at the top said the Fed Members have not discussed a “pause” in rates. Bottom line? Expect more uncertainty and volatility as it relates to rates.

Sound And Resilient

This is the term Fed Chair Powell used to describe the banking sector. Unfortunately, we are seeing more banks have issues. This week it was First Republic taken over by JP Morgan Chase and as of this writing PacWest was said to be “exploring strategic options.” The fear of banking contagion has elevated uncertainty in the financial markets. It’s not clear if and how many more banks will continue to have issues. Bottom line? The fear of this story has created a “safe haven” to trade into bonds where prices move higher, and rates move lower.

European Central Bank Hikes By Less

The European Central Bank (ECB) hiked their benchmark rate by .25%, the smallest since the start of their hiking cycle. Like our Fed, they too signaled they would be “data-dependent” going forward, leading markets to speculate a pause on future rate hikes.

Bottom line: The Federal Reserve is sending mixed messages on the future direction of rates. Meanwhile, long-term rates, which the Fed doesn’t control, are near their best levels in months and sense all the uncertainty in our economy will prompt the Fed to pause and potentially cut rates later this year. The incoming data and issues in the banking system will determine what happens next.

Looking Ahead

Expect market volatility to continue next week. The Consumer Price Index (inflation) will be reported. If this number comes in higher than expected, rates could rise. The opposite is true. Despite this being a backward-looking number, we will have Fed officials continue to speak and comment on the release and how they feel it impacts future Fed policy and interest rate decisions.

We’ve been getting a lot of questions about the new LLPA (loan level price adjustment) for Conforming loans and if people with worse credit will really get better rates than borrowers with excellent credit. The short answer is NO, and your clients should neverintentionally damage their credit. Surprise, surprise, there’s some entirely incorrect information circulating that your clients may be exposed to. Below is an explanation and FAQ’s:

What is changing?

Fannie May & Freddie Mac base pricing adjustments for credit scores & down payment are changing. Borrowers with a lower credit score & lower down payment will not be as heavily penalized. And, borrowers with best case scenario credit scores & down payment will receive less of a benefit than before. So, the difference in rates between best case credit profile vs. lower credit score will be less significant. These changes apply to every conforming loan funded by each & every mortgage company.

Does this mean borrowers with lower credit scores get better terms than those with higher credit score?

No. People will still be in better position with a better credit & more down payment. The difference between excellent & lower credit tiers will be less significant.

When does this go into effect?:

It’s been priced into rates for over a month now. The May 1st date is when these adjustments go into effect for the mortgages purchased on the secondary market by Fannie/Freddie. Banks knew this was coming, so these changes have already priced in and borrowers will not see any changes to rates over the next week, outside of the normal day to day bond/rate fluctuations.

What is the FHFA trying to achieve with these pricing adjustment?

We all know Fannie/Freddie’s mission to increase access to affordable housing. It’s always been their mission and it’s been a priority for the director of FHFA. The new director of the FHFA has been vocal in disapproval of the solutions provided by Franny and Freddie and she thinks more is required of them to increase access to affordable housing, and she thinks this will help increase access to affordable housing.

Is this a good idea and will it work?: We don’t like it but the whole world has to deal with it, so it is what it is at this point. We do not see these pricing changes moving the needle in making homeownership more attainable for more Americans because even after these changes a borrower with low 600’s credit score is still better off going with an FHA loan, and those who have done a great job managing credit are stuck a hair worse pricing. A better idea would be a campaign to educate people on how to manager credit; it’s not complicated and the information could be shared on something as simple as this one page I put together and have been sharing with clients for over a decade (see attached). WE (all of us on the real estate community) continue to be the front lines in educating the public on all things related to buying, investing, & enjoying real estate.

If you want to dig into the details, here are some example of scenarios that will be most affected: Attached is a matrix showing which scenarios have pricing improvements (green) vs. hits (red), relative to the old standard LLPA’s.

LTV’s in the 80% – 85% range are most significantly affected, so more borrowers in the ~19.99% – ~15% down might consider just doing 10%.

Cash-out refinances hits are mostly greater, unless you have top tier (>780) credit, or extremely low LTV (<30%). So, cash-out refi is actually a scenario where if credit is >780, pricing adjustments have improved.

Price improvements for 2 & 3 unit properties.

Price improvements for low LTV investment properties.

Vacation Homes & Investment Properties essentially priced the same now.

Good morning. The Fed must choose between two unpleasant options today. It’s a reminder of the high cost of weak bank oversight.

The Federal Reserve building. Haiyun Jiang/The New York Times

BY DAVID LEONHARDT

The New York Times

March 22, 2023

Inflation — or turmoil?

The Federal Reserve faces a difficult decision at its meeting that ends this afternoon: Should Fed officials raise interest rates in response to worrisome recent inflation data — and accept the risk of causing further problems for banks? Or should officials pause their rate increases — and accept the risk that inflation will remain high?

This dilemma is another reminder of the broad economic damage that banking crises cause. In today’s newsletter, I’ll first explain the Fed’s tough call and then look at one of the lessons emerging from the current banking turmoil. Above all, that turmoil is a reminder of the high costs of ineffective bank regulation, which has been a recurring problem in the U.S.

The Fed’s dilemma

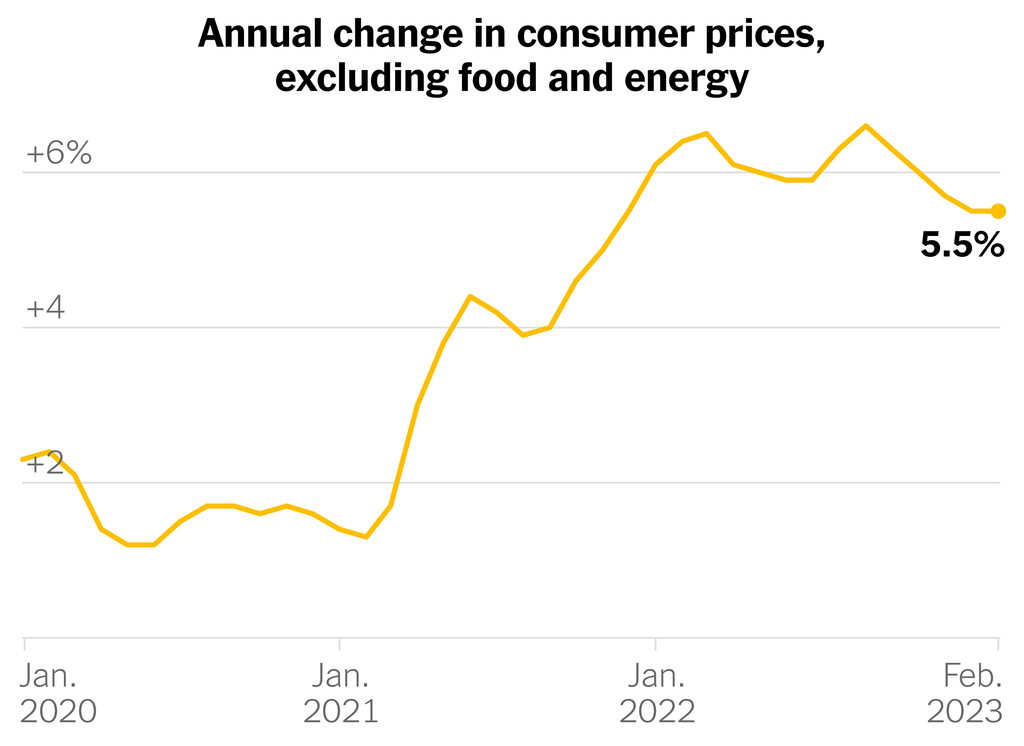

The trouble for the Fed is that there are excellent reasons for it to continue raising interest rates and excellent reasons for it to take a break. On the one hand, the economic data in recent weeks has suggested that inflation is not falling as rapidly as analysts expected. Average consumer prices are about 6 percent higher than a year ago, and forecasters expect the figure to remain above 3 percent for most of this year. That’s higher than Fed officials and many families find comfortable. For much of the 21st century, inflation has been closer to 2 percent.

An inflation rate that remains near 4 percent for an extended period is problematic for several reasons. It cuts into buying power and gives people reason to expect that inflation may stay high for years. They will then ask their employers for higher wages, potentially causing a spiral in which companies increase their prices to pay for the raises and inflation drifts even higher. Today’s tight job market, with unemployment near its lowest level since the 1960s, adds to these risks. The economy still seems to be running hotter than is sustainable.

This situation explains why Fed officials had originally planned to continue raising their benchmark interest rate at today’s meeting — thereby slowing the economy by increasing the cost of homes, cars and other items that people buy with debt. Some Fed officials favored a quarter-point increase, which would be identical to the increase at the Fed’s meeting last month. Others preferred a half-point increase, in response to the worrisome recent inflation data.

The banking troubles of the past two weeks scrambled these plans. Why? In addition to slowing the economy, higher interest rates depress the value of many financial assets (as these charts explain). Some bank executives did a poor job planning for these asset declines, and their balance sheets suffered. When customers became worried that the banks would no longer have enough money to return their deposits, a classic bank run ensued. It led to the collapse of Silicon Valley Bank and Signature Bank, and others remain in jeopardy.

If Fed officials continue raising their benchmark rate, they risk damaging the balance sheets of more banks and causing new bank runs. That’s why a half-point increase now seems less likely. Some economists (including The Times’s Paul Krugman) have urged the Fed to avoid any additional increases for now. Many analysts expect the Fed will compromise and raise the rate by a quarter point; Jason Furman, a former Obama administration official, leans toward that approach.

The decision is unavoidably fraught. The Fed must choose between potentially exacerbating problems in the financial markets and seeming to go soft on inflation.

Why bailouts happen

All of which underscores the high cost of banking crises. In most industries, a company’s collapse doesn’t cause cascading economic problems. In the financial markets, the collapse of one firm can lead to a panic that feeds on itself. Investors and clients start withdrawing their money. A recession, or even a depression, can follow.

These consequences are the reason that government officials bail out banks more frequently than other businesses. Bailouts, of course, have huge downsides: They typically use taxpayer money (or other banks’ money) to subsidize affluent bank executives who failed at their jobs. “Nobody is as privileged in the entire economy,” Anat Admati, a finance professor at Stanford University’s business school, told me.

During a crisis, bailouts can be unavoidable because of the economic risks from bank collapses. The key question, then, is how to regulate banks rigorously enough to minimize the number of necessary bailouts.

Over the past few decades, the U.S. has failed to do so. After the financial crisis of 2007-9, policymakers tightened the rules through the Dodd-Frank Act. But Congress and the Trump administration loosened oversight for midsize banks in 2018 — and Silicon Valley Bank and Signature Bank were two of the firms that stood to benefit.

As complicated as finance can be, the basic principles behind bank regulation are straightforward. Banks require special scrutiny from the government because they may receive special benefits from taxpayers during a crisis. This scrutiny includes limits on the risks that banks can take and requirements that they keep enough money in reserve to survive most foreseeable crises. “You make sure they have enough to pay,” as Admati put it.

Bank executives and investors often bristle at such rules because they reduce returns. Money held in reserve, after all, cannot be invested elsewhere and earn big profits. It also can’t go poof when hard times arrive.

Quite an exciting week and a half and I have some additional commentary to share in addition to this week’s MMG update (below). Silicon Valley Bank failed for several reasons, and while it is of course the bank’s responsibility to manage risk, it was the Fed being late to the game in hiking the Fed Funds rate and then hiking so much in such a short period of time that pushed SVB’s bond holdings so significantly underwater. SVB held a large position in government bonds, which are generally considered the world’s safest parking for money, and those bond yields were as close to zero as they’ve ever been. A bond’s value on the market can be determine primarily by; it’s yield the maturity. So, when the Fed hikes rates rather drastically in a such a short period of time, new bonds become available with a dramatically higher yield, in comparison to those bonds SVB & others were buying just a handful of months earlier – with a relatively small difference in maturity. This put the value of those bonds underwater, but that’s not what caused the problem. If SVB had been able to simply hold those bonds to maturity, there would have been no loss. However, after some prominent VC’s yelled fire in the theatre & sparked a run on the bank with depositors to pulling money out, SVB quickly tried to raise capital to cover those withdrawals, and when they couldn’t raise money, they were forced to sell those underwater bonds to cover the withdrawals. Yes, there are some things SVB should have done differently, like fill that Risk Management Officer role that sat vacant tail end of last year, and hold less in such low yield bonds, but it was the Fed’s concentrated rate hikes that pushed those low yield young in maturity bonds underwater. The bank failure was backstopped by the Federal government working with FDIC to use funds from the FDIC insurance pool to guarantee all depositors would be made whole. No tax payers dollars were used for this bail out, bank executives are being held accountable for poor risk management, and many who are often most critical of government intervention in markets agree, the administration & FDIC did an excellent job solving this potential crisis.

With respect to how all this this impacts mortgage rates, US bonds & treasuries are still the world’s safest parking for money, so SVB inspired concern surrounding regional banks has created a flight to safety with investment capital going into bonds, that demand pushes bonds prices up & yields/rates down. As a result, the past week has seen the most significant improvement to mortgage rates since the November & December CPI (inflation) reports came in lower than expected. Last week’s (3/14) CPI report came in exactly at market expectations of 6.0%, which allowed mortgage rates to hold on to gains. This week’s Fed meeting is another potentially high impact event. Wild week, but with respect to mortgage rates, they improved a bit last week and we expect inflation to continue gradually decrease and we still expect mortgage rates to be a little lower by end of this year – best guess would be mid/low 5%’.s

This past week, home loan rates improved to their lowest levels in a month in response to the closures of Silicon Valley Bank (SVB) and Signature Bank. Let’s walk through what happened as we approach the Fed Meeting next week.

It’s important to remember that bonds enjoy bad news, so when word broke earlier this week that SVB was shuttered by the FDIC, home loan rates improved to their best level in six weeks. At the same time, the 2-year Note yield, which tracks Fed rate hike activity, plummeted from over 5.00% to under 4.00% in just a couple of days. This was an epic decline in rates not seen even after 9/11 or the Great Recession.

The good news (in the case of SVB and even Signature) is that bad management, failure to manage interest rate risk and a widespread desire for depositors to gain access to their funds (bank run) is what caused these banks to shutter.

In response, the Federal Reserve immediately created a line of credit and an implicit backstop to protect any depositors from any losses. This was good news and will hopefully limit any further fallout in the banking sector.

So, what does the Fed do with rates now that we have high uncertainty and contagion risk in the banking sector?

Stability > Inflation

Seeing that one reason SVB failed was in response to a rapid rise in interest rates, there is increased pressure for the Fed to limit rate hikes going forward and regain stability in the financial sector.

Just last week there was a high probability the Fed would raise rates by .50. Now just days later, there is a 75% chance of a .25% and a 25% chance the Fed doesn’t hike rates at all.

Next week’s Fed Meeting and press conference will hopefully have the markets feeling that the Fed is going to take every measure possible to ensure stability while they closely watch the pace of inflation decline.

Housing Numbers OK

It wasn’t all bad news this week. Housing numbers for February highlighted the little rate relief we saw in January and brought some optimism into February. Both Housing Starts (which is putting the shovel in the ground), and Permits (a leading indicator of future building), came in better than expectations.

This bodes well for housing in the months ahead, especially combined with the rate relief we are experiencing.

Bottom line:This week’s news in banking has changed everything as it relates to the Fed and rate hikes. The markets are suggesting the Fed will be cutting rates in the second half of the year which is a big change from the rate outlook just days ago.

Looking Ahead

Next week brings the Fed Meeting and monetary policy decision. As we shared, it appears the Fed is only going to raise rates by .25%, rather than .50% to foster stability in the financial markets and avoid contagion in the banking sector. What the Fed says will be important in bringing calm to the markets during this uncertain moment.

Change is the only constant in life. After two years of a COVID-fueled buying frenzy that produced stratospheric price spikes across all segments of the market, 2022 brought a bucket of icy lake water on the head. A dramatic reversal of economic conditions fueled by the Ukrainian conflict, historic interest rate hikes, a crypto collapse, and the erosion of equities rippled through Tahoe real estate. For the first time since COVID, we saw a noticeable lack of urgency as buyers were willing to wait on investing in vacation homes. By mid-summer, both supply and days-on-market had distinctly increased. Gone were the days of multiple offers within days of listing homes and the manic-ness we experienced since the pandemic onset. By the third quarter, we saw a palpable calm in luxury real estate sales. In fact, only 11 single-family lakefront homes between Rubicon Bay and Incline Village sold all year, the lowest we have seen since before our reporting began in 2006. Yet, median price has been slow to respond. As a result, in 2022, each micro-region (with the exception of lakefronts due to small sample size), saw median price reach historic highs, while sales volume decreased significantly. The disparity between median price and demand, alongside uncertain market conditions, continues to contribute to buyers willing to remain on standby, waiting for market corrections and for economic indicators to improve confidence.

As sellers reset to the new normal, we expect buyers to start to again pull their paddles from beneath their chairs in 2023. For buyers who have been patiently awaiting value opportunities, 2023 should present well. While the selling environment is not as favorable as it has been over the past few years, sellers can still take advantage of the historic run-up in pricing from COVID. However, it will be imperative that sellers adjust expectations on pricing and time on market. As we close the chapter on the COVID-driven real estate binge, the winds of change will still blow in opportunities around Lake Tahoe.

Points of Interest: January – December 2022

Single family homes sold decreased 19% year over year.

Median price increased 7% year over year and is on a 7-year growth trend.

Sales volume reached a 8-year low. Median price reached an historic high.

210 of 903 homes (23%) sold over $2 million.

Points of Interest: January – December 2022

Single family homes sold decreased 10% year over year

Median price increased 24% year over year and is on a 5-year growth trend.

Sales volume reached a 6-year low. Median price reached an historic high.

In the first three quarters of 2022, each micro-region saw a decrease in the number of single-family homes sold. While some micro-regions have continued to see slow growth in median price, other micro-regions have started to see a decline in pricing.

The combination of the decline in sales volume and the shifting of price indicates that market activity is slowing. The expectation is that the median price will follow but is slower to react, as sellers still aim for the pricing the market waws garnering in the first half of the year.

Increased interest rates may also impact buyer activity. Most significantly, we see a noticeable lack of urgency in stark contrast to the buying frenzy of COVID years, as people continue to watch the market and economic indicators. Buyers who have been sitting on the sidelines may find their opportunity to take advantage of their new leverage.

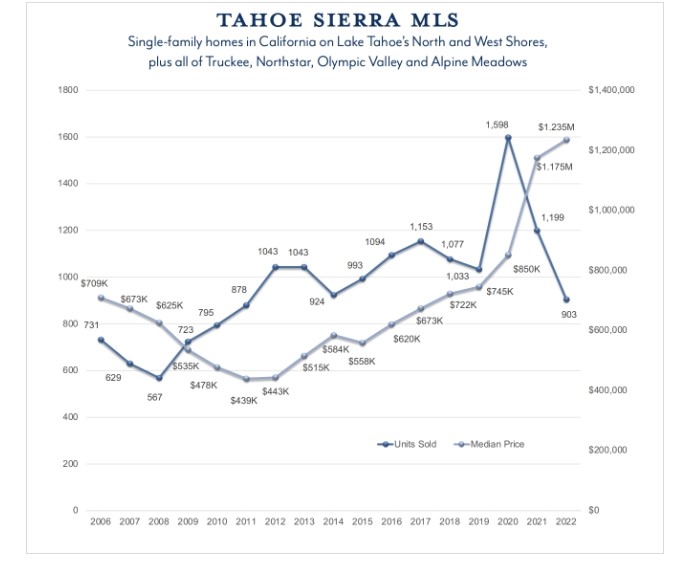

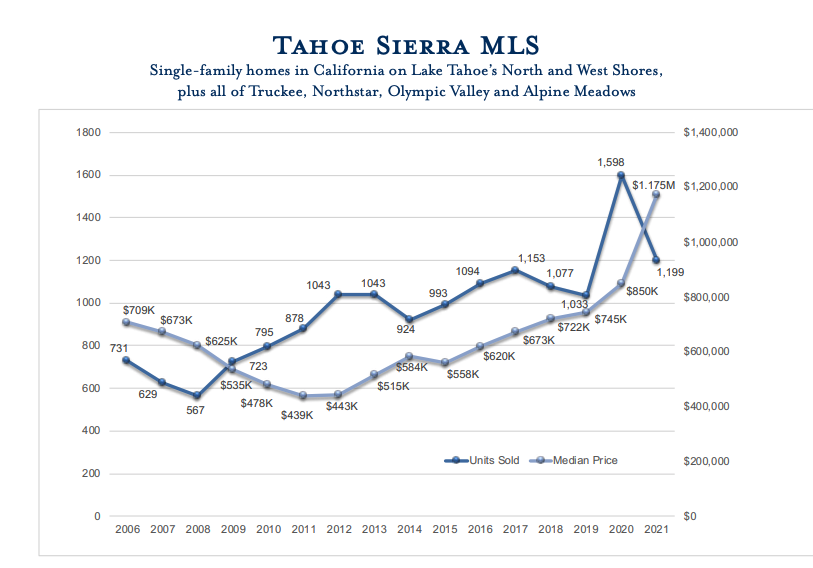

Tahoe Sierra MLS

Single-family homes in California on Lake Tahoe’s North and West Shores, plus all of Truckee, Northstar, Olympic Valley and Alpine Meadows.

Points of Interest

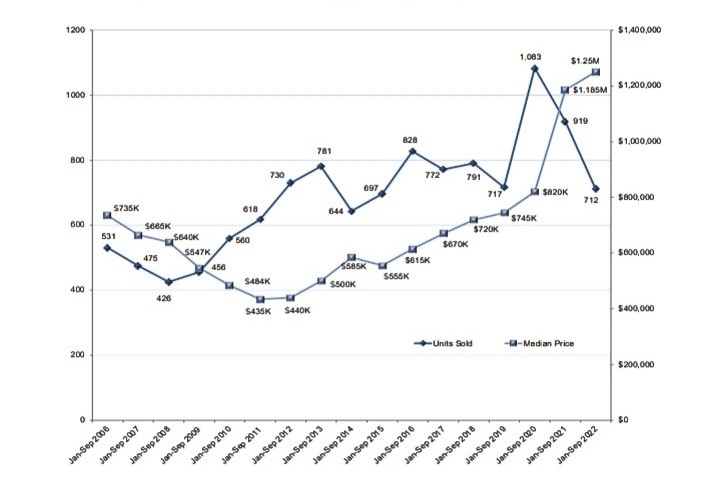

Single-family homes sold decreased 23% year over year.

Median price increased 5% year over year and is on a 7-year growth trend.

Sales volume reached a 6-year low.

170 of 712 homes (24%) sold over $2 million.

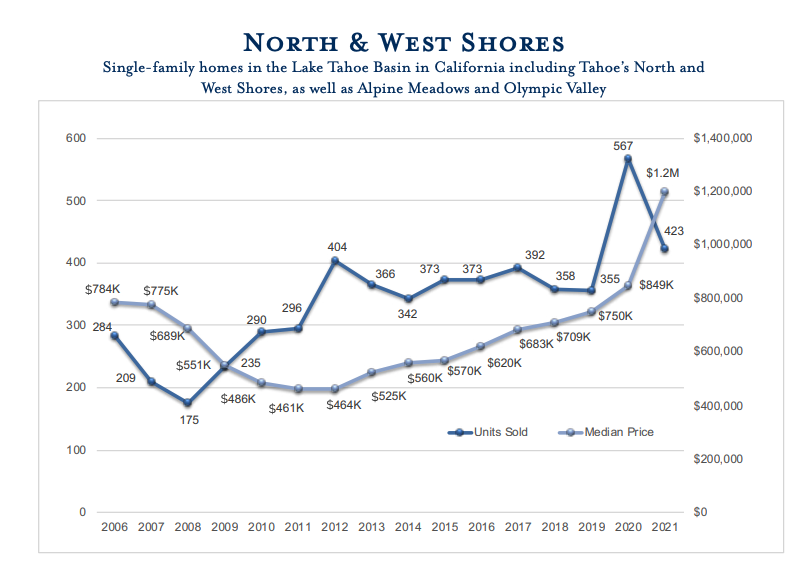

North & West Shores

Single-family homes in the Lake Tahoe Basin in California including Tahoe’s North and West Shores, as well as Alpine Meadows and Olympic Valley.

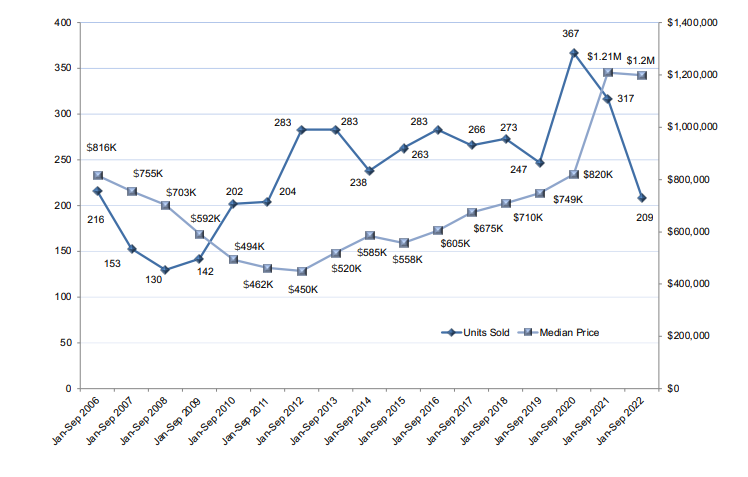

Points of Interest

Single-family homes sold decreased 34% year over year.

Median price decreased 1% year over year.

Sales volume reached a 10-year low.

49 of 209 homes (23%) sold over $2 million.

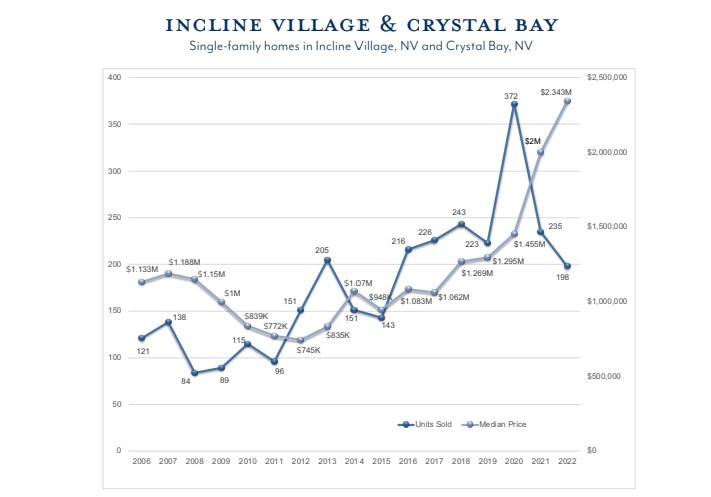

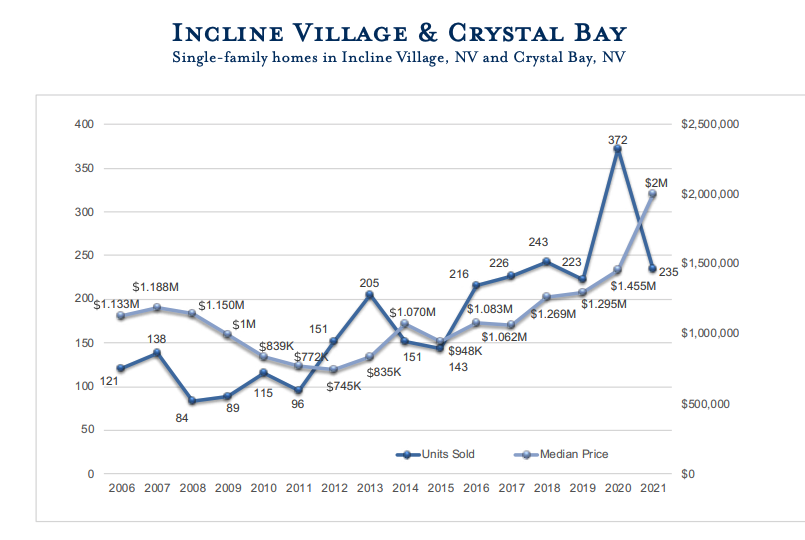

Incline Village & Crystal Bay

Single-family homes in Incline Village, NV and Crystal Bay, NV.

Points of Interest

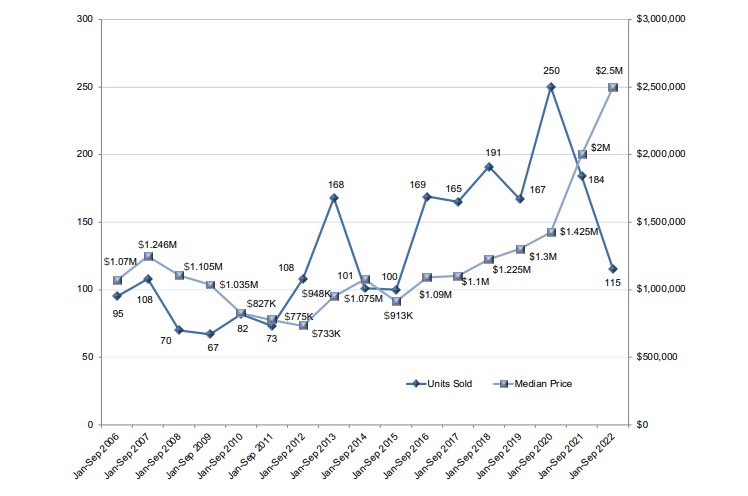

Single-family homes sold decreased 38% year over year.

Median price increased 25% year over year and is on a 7-year growth trend.

Sales volume reached a 5-year low.

74 of 115 homes (64%) sold for over $2 million.

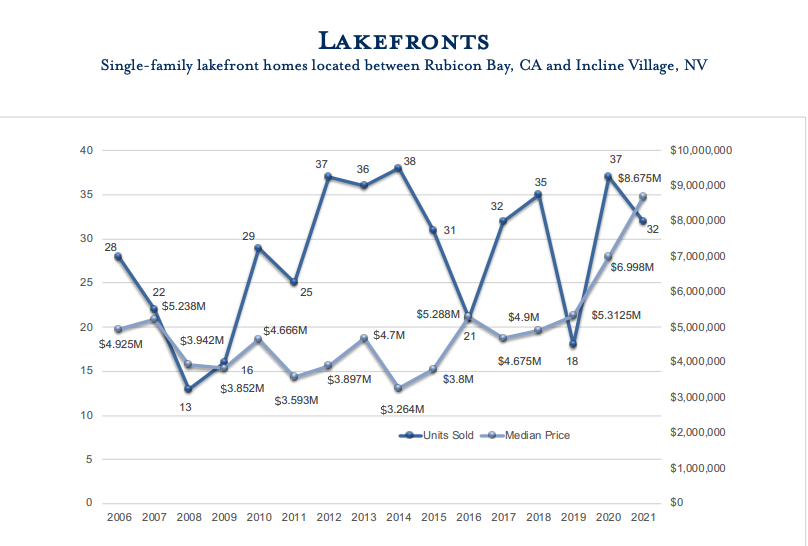

Lakefronts

Single-family lakefront homes located between Rubicon Bay, CA and Incline Village, NV.

Points of Interest

Single-family homes sold decreased 67% year over year.

Median price decreased 28% year over year.

Sales volume reached a record low (16 years of data).

8 of 8 homes (100%) sold for over $2 million.

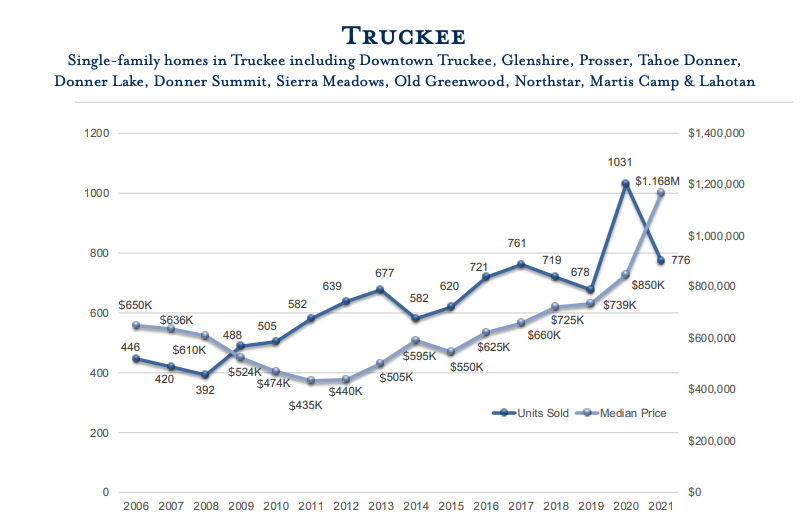

Truckee

Single-family homes in Truckee including Downtown Truckee, Glenshire, Prosser, Tahoe-Donner, Donner Lake, Donner Summit, Sierra Meadows, Old Greenwood, Northstar, Martis Camp & Lahontan.\

Points of Interest

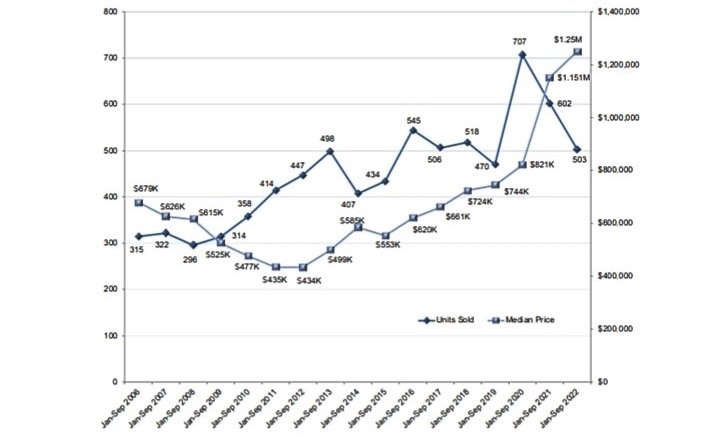

Single-family homes sold decreased by 16% year over year.

Median price increased by 9% year over year and is on a 7-year growth trend.

Median price reached an historic high. Sales volume is the second lowest in 6 years.

Last year at this time, we reported that 2020 was an historic year in Lake Tahoe real estate, showcasing dramatic and unprecedented activity as a result of the pandemic shifting buying behavior and accessibility. In 2020, our Year End Market Report highlighted a massive spike in sales volume alongside a noticeable increase in median price, with both reaching record highs in all microregions (with the exception of lakefronts, where sales volume fell one home below the record). This year, we are seeing median prices once again reaching historic highs in all micro-regions, although by a much larger increase, with the minimum being a 24% increase in median price year over year (on top of the previous record high, that is!). The difference is that in 2021, all micro-regions are showing a decrease in sales volume, by a minimum of 14% and as high as 37% year over year. The decrease in sales volume may be due to limited inventory available, however it also may be indicative of the market reaching our threshold in pricing. On Lake Tahoe’s North & West Shores, median price has been on a 10-year upwards trajectory and this year alone saw a 41% increase in median price. We look forward to 2022 to determine if these trends are sustainable, or if we will begin to see a plateau as the market attempts to correct itself.

2021 Market Recap

Single-family homes sold decreased 25% year over year.

Median price increased 38% year over year and is on a 6-year growth trend.

Median price reached an historic high.

236 of 1,199 homes (20%) sold over $2 million.

North & West Shore Recap

Single-family homes sold decreased 25% year over year.

Median price increased 41% year over year and is on a 10-year growth trend.

Median price reached an historic high.

83 of 423 homes (20%) sold for over $2 million.

Incline Village & Crystal Bay

Single-family homes sold decreased 37% year over year.

Median price increased 37% year over year and is on a 4-year growth trend.

Median price reached an historic high.

118 of 235 homes (50%) sold for over $2 million.

Lakefronts

Single-family homes sold decreased 14% year over year.

Median price increased 24% year over year and reached an historic high.

32 of 32 homes (100%) sold for over $2 million.

Truckee

Single-family homes sold decreased by 25% year over year.

Median price increased by 37% year over year and is on a 6-year growth trend.