This past week the Federal Reserve raised rates for the 10th time in a little over a year. Let’s discuss what happened as we await yet another Fed rate hike next Wednesday.

As we expected, the Federal Reserve raised the Fed Funds Rate to a range of 5.00% – 5.25%. Remember, this interest rate affects short-term loans like credit cards, autos, and home equity lines of credit.

The big question is whether this will be the last hike. When the Fed statement was released, the markets believed the Fed was signaling a pause by omitting the following line from the previous statement: “The Committee anticipates that some additional policy firming may be appropriate.”

However, shortly after the statement was released, Fed Chair Powell hosted a press conference and right at the top said the Fed Members have not discussed a “pause” in rates. Bottom line? Expect more uncertainty and volatility as it relates to rates.

Sound And Resilient

This is the term Fed Chair Powell used to describe the banking sector. Unfortunately, we are seeing more banks have issues. This week it was First Republic taken over by JP Morgan Chase and as of this writing PacWest was said to be “exploring strategic options.” The fear of banking contagion has elevated uncertainty in the financial markets. It’s not clear if and how many more banks will continue to have issues. Bottom line? The fear of this story has created a “safe haven” to trade into bonds where prices move higher, and rates move lower.

European Central Bank Hikes By Less

The European Central Bank (ECB) hiked their benchmark rate by .25%, the smallest since the start of their hiking cycle. Like our Fed, they too signaled they would be “data-dependent” going forward, leading markets to speculate a pause on future rate hikes.

Bottom line: The Federal Reserve is sending mixed messages on the future direction of rates. Meanwhile, long-term rates, which the Fed doesn’t control, are near their best levels in months and sense all the uncertainty in our economy will prompt the Fed to pause and potentially cut rates later this year. The incoming data and issues in the banking system will determine what happens next.

Looking Ahead

Expect market volatility to continue next week. The Consumer Price Index (inflation) will be reported. If this number comes in higher than expected, rates could rise. The opposite is true. Despite this being a backward-looking number, we will have Fed officials continue to speak and comment on the release and how they feel it impacts future Fed policy and interest rate decisions.

We’ve been getting a lot of questions about the new LLPA (loan level price adjustment) for Conforming loans and if people with worse credit will really get better rates than borrowers with excellent credit. The short answer is NO, and your clients should neverintentionally damage their credit. Surprise, surprise, there’s some entirely incorrect information circulating that your clients may be exposed to. Below is an explanation and FAQ’s:

What is changing?

Fannie May & Freddie Mac base pricing adjustments for credit scores & down payment are changing. Borrowers with a lower credit score & lower down payment will not be as heavily penalized. And, borrowers with best case scenario credit scores & down payment will receive less of a benefit than before. So, the difference in rates between best case credit profile vs. lower credit score will be less significant. These changes apply to every conforming loan funded by each & every mortgage company.

Does this mean borrowers with lower credit scores get better terms than those with higher credit score?

No. People will still be in better position with a better credit & more down payment. The difference between excellent & lower credit tiers will be less significant.

When does this go into effect?:

It’s been priced into rates for over a month now. The May 1st date is when these adjustments go into effect for the mortgages purchased on the secondary market by Fannie/Freddie. Banks knew this was coming, so these changes have already priced in and borrowers will not see any changes to rates over the next week, outside of the normal day to day bond/rate fluctuations.

What is the FHFA trying to achieve with these pricing adjustment?

We all know Fannie/Freddie’s mission to increase access to affordable housing. It’s always been their mission and it’s been a priority for the director of FHFA. The new director of the FHFA has been vocal in disapproval of the solutions provided by Franny and Freddie and she thinks more is required of them to increase access to affordable housing, and she thinks this will help increase access to affordable housing.

Is this a good idea and will it work?: We don’t like it but the whole world has to deal with it, so it is what it is at this point. We do not see these pricing changes moving the needle in making homeownership more attainable for more Americans because even after these changes a borrower with low 600’s credit score is still better off going with an FHA loan, and those who have done a great job managing credit are stuck a hair worse pricing. A better idea would be a campaign to educate people on how to manager credit; it’s not complicated and the information could be shared on something as simple as this one page I put together and have been sharing with clients for over a decade (see attached). WE (all of us on the real estate community) continue to be the front lines in educating the public on all things related to buying, investing, & enjoying real estate.

If you want to dig into the details, here are some example of scenarios that will be most affected: Attached is a matrix showing which scenarios have pricing improvements (green) vs. hits (red), relative to the old standard LLPA’s.

LTV’s in the 80% – 85% range are most significantly affected, so more borrowers in the ~19.99% – ~15% down might consider just doing 10%.

Cash-out refinances hits are mostly greater, unless you have top tier (>780) credit, or extremely low LTV (<30%). So, cash-out refi is actually a scenario where if credit is >780, pricing adjustments have improved.

Price improvements for 2 & 3 unit properties.

Price improvements for low LTV investment properties.

Vacation Homes & Investment Properties essentially priced the same now.

Good morning. The Fed must choose between two unpleasant options today. It’s a reminder of the high cost of weak bank oversight.

The Federal Reserve building. Haiyun Jiang/The New York Times

BY DAVID LEONHARDT

The New York Times

March 22, 2023

Inflation — or turmoil?

The Federal Reserve faces a difficult decision at its meeting that ends this afternoon: Should Fed officials raise interest rates in response to worrisome recent inflation data — and accept the risk of causing further problems for banks? Or should officials pause their rate increases — and accept the risk that inflation will remain high?

This dilemma is another reminder of the broad economic damage that banking crises cause. In today’s newsletter, I’ll first explain the Fed’s tough call and then look at one of the lessons emerging from the current banking turmoil. Above all, that turmoil is a reminder of the high costs of ineffective bank regulation, which has been a recurring problem in the U.S.

The Fed’s dilemma

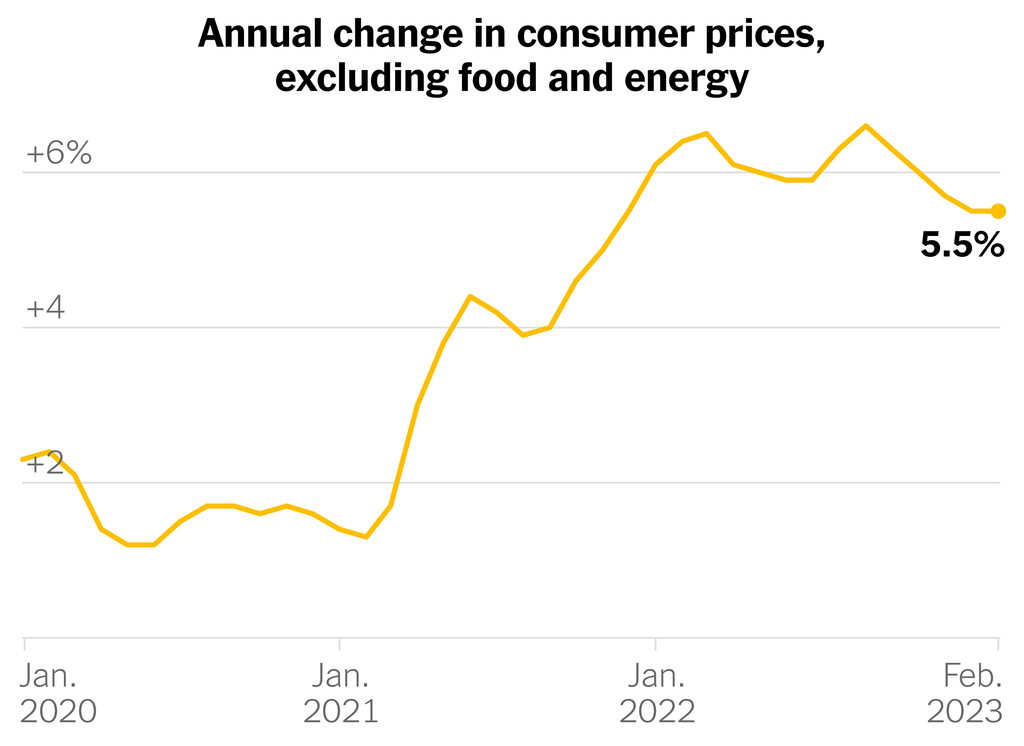

The trouble for the Fed is that there are excellent reasons for it to continue raising interest rates and excellent reasons for it to take a break. On the one hand, the economic data in recent weeks has suggested that inflation is not falling as rapidly as analysts expected. Average consumer prices are about 6 percent higher than a year ago, and forecasters expect the figure to remain above 3 percent for most of this year. That’s higher than Fed officials and many families find comfortable. For much of the 21st century, inflation has been closer to 2 percent.

An inflation rate that remains near 4 percent for an extended period is problematic for several reasons. It cuts into buying power and gives people reason to expect that inflation may stay high for years. They will then ask their employers for higher wages, potentially causing a spiral in which companies increase their prices to pay for the raises and inflation drifts even higher. Today’s tight job market, with unemployment near its lowest level since the 1960s, adds to these risks. The economy still seems to be running hotter than is sustainable.

This situation explains why Fed officials had originally planned to continue raising their benchmark interest rate at today’s meeting — thereby slowing the economy by increasing the cost of homes, cars and other items that people buy with debt. Some Fed officials favored a quarter-point increase, which would be identical to the increase at the Fed’s meeting last month. Others preferred a half-point increase, in response to the worrisome recent inflation data.

The banking troubles of the past two weeks scrambled these plans. Why? In addition to slowing the economy, higher interest rates depress the value of many financial assets (as these charts explain). Some bank executives did a poor job planning for these asset declines, and their balance sheets suffered. When customers became worried that the banks would no longer have enough money to return their deposits, a classic bank run ensued. It led to the collapse of Silicon Valley Bank and Signature Bank, and others remain in jeopardy.

If Fed officials continue raising their benchmark rate, they risk damaging the balance sheets of more banks and causing new bank runs. That’s why a half-point increase now seems less likely. Some economists (including The Times’s Paul Krugman) have urged the Fed to avoid any additional increases for now. Many analysts expect the Fed will compromise and raise the rate by a quarter point; Jason Furman, a former Obama administration official, leans toward that approach.

The decision is unavoidably fraught. The Fed must choose between potentially exacerbating problems in the financial markets and seeming to go soft on inflation.

Why bailouts happen

All of which underscores the high cost of banking crises. In most industries, a company’s collapse doesn’t cause cascading economic problems. In the financial markets, the collapse of one firm can lead to a panic that feeds on itself. Investors and clients start withdrawing their money. A recession, or even a depression, can follow.

These consequences are the reason that government officials bail out banks more frequently than other businesses. Bailouts, of course, have huge downsides: They typically use taxpayer money (or other banks’ money) to subsidize affluent bank executives who failed at their jobs. “Nobody is as privileged in the entire economy,” Anat Admati, a finance professor at Stanford University’s business school, told me.

During a crisis, bailouts can be unavoidable because of the economic risks from bank collapses. The key question, then, is how to regulate banks rigorously enough to minimize the number of necessary bailouts.

Over the past few decades, the U.S. has failed to do so. After the financial crisis of 2007-9, policymakers tightened the rules through the Dodd-Frank Act. But Congress and the Trump administration loosened oversight for midsize banks in 2018 — and Silicon Valley Bank and Signature Bank were two of the firms that stood to benefit.

As complicated as finance can be, the basic principles behind bank regulation are straightforward. Banks require special scrutiny from the government because they may receive special benefits from taxpayers during a crisis. This scrutiny includes limits on the risks that banks can take and requirements that they keep enough money in reserve to survive most foreseeable crises. “You make sure they have enough to pay,” as Admati put it.

Bank executives and investors often bristle at such rules because they reduce returns. Money held in reserve, after all, cannot be invested elsewhere and earn big profits. It also can’t go poof when hard times arrive.

Quite an exciting week and a half and I have some additional commentary to share in addition to this week’s MMG update (below). Silicon Valley Bank failed for several reasons, and while it is of course the bank’s responsibility to manage risk, it was the Fed being late to the game in hiking the Fed Funds rate and then hiking so much in such a short period of time that pushed SVB’s bond holdings so significantly underwater. SVB held a large position in government bonds, which are generally considered the world’s safest parking for money, and those bond yields were as close to zero as they’ve ever been. A bond’s value on the market can be determine primarily by; it’s yield the maturity. So, when the Fed hikes rates rather drastically in a such a short period of time, new bonds become available with a dramatically higher yield, in comparison to those bonds SVB & others were buying just a handful of months earlier – with a relatively small difference in maturity. This put the value of those bonds underwater, but that’s not what caused the problem. If SVB had been able to simply hold those bonds to maturity, there would have been no loss. However, after some prominent VC’s yelled fire in the theatre & sparked a run on the bank with depositors to pulling money out, SVB quickly tried to raise capital to cover those withdrawals, and when they couldn’t raise money, they were forced to sell those underwater bonds to cover the withdrawals. Yes, there are some things SVB should have done differently, like fill that Risk Management Officer role that sat vacant tail end of last year, and hold less in such low yield bonds, but it was the Fed’s concentrated rate hikes that pushed those low yield young in maturity bonds underwater. The bank failure was backstopped by the Federal government working with FDIC to use funds from the FDIC insurance pool to guarantee all depositors would be made whole. No tax payers dollars were used for this bail out, bank executives are being held accountable for poor risk management, and many who are often most critical of government intervention in markets agree, the administration & FDIC did an excellent job solving this potential crisis.

With respect to how all this this impacts mortgage rates, US bonds & treasuries are still the world’s safest parking for money, so SVB inspired concern surrounding regional banks has created a flight to safety with investment capital going into bonds, that demand pushes bonds prices up & yields/rates down. As a result, the past week has seen the most significant improvement to mortgage rates since the November & December CPI (inflation) reports came in lower than expected. Last week’s (3/14) CPI report came in exactly at market expectations of 6.0%, which allowed mortgage rates to hold on to gains. This week’s Fed meeting is another potentially high impact event. Wild week, but with respect to mortgage rates, they improved a bit last week and we expect inflation to continue gradually decrease and we still expect mortgage rates to be a little lower by end of this year – best guess would be mid/low 5%’.s

This past week, home loan rates improved to their lowest levels in a month in response to the closures of Silicon Valley Bank (SVB) and Signature Bank. Let’s walk through what happened as we approach the Fed Meeting next week.

It’s important to remember that bonds enjoy bad news, so when word broke earlier this week that SVB was shuttered by the FDIC, home loan rates improved to their best level in six weeks. At the same time, the 2-year Note yield, which tracks Fed rate hike activity, plummeted from over 5.00% to under 4.00% in just a couple of days. This was an epic decline in rates not seen even after 9/11 or the Great Recession.

The good news (in the case of SVB and even Signature) is that bad management, failure to manage interest rate risk and a widespread desire for depositors to gain access to their funds (bank run) is what caused these banks to shutter.

In response, the Federal Reserve immediately created a line of credit and an implicit backstop to protect any depositors from any losses. This was good news and will hopefully limit any further fallout in the banking sector.

So, what does the Fed do with rates now that we have high uncertainty and contagion risk in the banking sector?

Stability > Inflation

Seeing that one reason SVB failed was in response to a rapid rise in interest rates, there is increased pressure for the Fed to limit rate hikes going forward and regain stability in the financial sector.

Just last week there was a high probability the Fed would raise rates by .50. Now just days later, there is a 75% chance of a .25% and a 25% chance the Fed doesn’t hike rates at all.

Next week’s Fed Meeting and press conference will hopefully have the markets feeling that the Fed is going to take every measure possible to ensure stability while they closely watch the pace of inflation decline.

Housing Numbers OK

It wasn’t all bad news this week. Housing numbers for February highlighted the little rate relief we saw in January and brought some optimism into February. Both Housing Starts (which is putting the shovel in the ground), and Permits (a leading indicator of future building), came in better than expectations.

This bodes well for housing in the months ahead, especially combined with the rate relief we are experiencing.

Bottom line:This week’s news in banking has changed everything as it relates to the Fed and rate hikes. The markets are suggesting the Fed will be cutting rates in the second half of the year which is a big change from the rate outlook just days ago.

Looking Ahead

Next week brings the Fed Meeting and monetary policy decision. As we shared, it appears the Fed is only going to raise rates by .25%, rather than .50% to foster stability in the financial markets and avoid contagion in the banking sector. What the Fed says will be important in bringing calm to the markets during this uncertain moment.

The ebb and flow of the real estate business can be affected by the seasons, the economy and more. Here’s how to weather the slow times while building your business.

I sell real estate in Lake Tahoe, a seasonal and second-homeowner destination. Due to our unique market, I’ve become accustomed to the inevitable slowdowns every fall and spring.

At the beginning of my career, it wasn’t easy to normalize the downtime and find productivity in my business, even without clients. I would become anxious, stressed and paranoid until I found ways to utilize my free time efficiently.

Below are a few steps that you can implement in your business when you’re low on clients:

1. Remind yourself that every single agent, even the most successful agents making millions of dollars every year, experience lulls in their business

We’ll have highs, lows and everything in between. So while you’re having your best year, I could be having my worst year. That doesn’t mean you won’t ever sell a house again; it just means that the timing of your clients, or future clients, hasn’t reached the inflection point of a sale yet.

As hard as it is to not compare yourself to others or desperately watch the sales tick away in the MLS without your name, work on staying grounded and believing that your time will come. A positive mindset will work wonders for you, while a negative mindset can negatively impact your work.

2. Work on your business instead of in it

The downtime is a great time to master your systems, become clear on what is working and what isn’t, home in on your farms, get to know the behavior of your farms and more. The downtime allows you the gift of time, which is when most of us can be the most creative.

I like to start each day by sitting in silence for 20 minutes. I put a timer on my phone and don’t pick up any electronics during those 20 minutes. I simply sit with my thoughts and let the creative juices flow. I have a journal dedicated to my “thinking time,” I journal down all of my ideas once the timer goes off. I have my best (and most fun) marketing ideas during this time.

3. Plan events or create a value proposition for past, present or future clients

Planning events can be time-consuming, so downtime is the perfect opportunity to work on one. Contrary to popular belief, you do not need to shell out a large chunk of cash to host a successful event. In fact, you can do it for free.

Recently, we hosted a free, first-time homebuyer seminar with a local mortgage broker at a brewery in town. We used social media to market our event, had the space donated to us and put together the slides ourselves. We had over 30 attendees, many of whom converted into leads.

The best part? We’ve been able to help our first-time, local homebuyers buy a home in Tahoe.

By creating and hosting events such as this, you’re helping others, first and foremost, but you’re also adding more familiarity to your name and what you do, which is what marketing is all about.

4. Spend time with people you love and your past clients

My favorite type of lead is a referral from someone I know, like and trust. There is no greater honor than being introduced to a friend’s friend based on their confidence in me as their Realtor. The best way to gain that trust is simply by spending time with people.

Ask friends out to coffee, mention your business and what you’re doing, and ask them about their business. Be genuine.

If you don’t have the funds to take someone out to coffee, ask them to go on a walk, start a book club or tailor it to their and your personal interests.

These meaningful moments with people go a long way. The more time you spend working on the relationships in your life, the more people will think of you anytime the word real estate is mentioned.

5. Ensure all of your online profiles and social media channels are up to date

This one is self-explanatory, but make sure your bio is correct on every real estate site, add all of your past sales, ask past clients for reviews, and do your best to stay as relevant as you can online. Your online presence makes a difference, and finding time to dedicate to this is essential.

While it may be hard to mentally adjust to having very few clients, I hope you can look at it as a positive with unlimited potential to unlock the next phase of your business. If you are running at all cylinders all of the time, you won’t be able to ensure the mechanics of your business are still operating at full capacity.

I like to think of real estate like a conveyor belt: If you become too focused on the end of the line (closings, current transactions, etc.) you won’t have anything to work on once you reach the end because you haven’t been reloading the belt with new items (i.e. new clients and escrows). Therefore, to reach your full potential in this business, you must master the conveyor belt from start to finish.

After last week’s surprisingly strong Jobs Report, Fed Chair Jerome Powell spoke about the economy and direction of rates. Let’s walk through what happened and what to watch in the week ahead.

“The strong Jobs Report shows you why we think this will be a process that takes a significant period of time.” Fed Chair Powell 2/7/23.

BY EPHRAIM SCHWARTZ

Partner, Mortgage Consultant CMPS

O’Dette Mortgage Group

February 14, 2023

The Federal Reserve has a dual mandate, which is to maintain price stability (inflation) and promote maximum employment. On the inflation front, it appears inflation has indeed peaked and is on the decline. The Fed Chair reiterated the “disinflationary process” has begun. This is a positive development for the economy, housing, and long-term rates.

On the labor market front of the Fed’s mandate, the Fed in its desire to slow demand and thus inflation, wants to see some unemployment. The good news/bad news? Last week, the Bureau of Labor Statistics (BLS) reported the unemployment rate at 3.4%, the lowest in 53 years…that is good news. The bad news is it means the Fed will look to raise rates by .25% in March and another .25% in May, thereby lifting the Fed Funds Rate above 5.00%.

This renewed outlook for a higher Fed Funds Rate has elevated uncertainty and volatility in long-term rates, which move up and down based on economic conditions and inflation, both of which are easing and a reason why long-term rates are lower than short-term rates.

“Likely to see some softening in labor market conditions” – Powell

This is a reasonable assumption considering the number of planned layoffs announced this year, while we sit at multi-decade low unemployment, it seems like up is the only direction for unemployment.

Soft Landing Back in Play

Due to the current strength of the labor market, there is a growing chance the Fed can raise rates and lower inflation towards its 2.00% target without triggering a deep recession.

History has shown that recessions do not take place with unemployment at 4% or below without some sort of surprise shock to the economy.

Let’s hope the Fed is not too successful in “creating” unemployment because if it quickly rises, the idea of a soft economic landing could go away quickly too.

3.70%

As we mentioned, long-term rates have responded negatively to last week’s strong jobs report, because good news is bad news for bonds and rates. The 10-yr Note touched 3.33% last Thursday and touched 3.70% just a few days later. However, rates remain beneath where the 10-yr yield opened 2023 at 3.85%.

“We are going to react to the data” – Powell

Here the Fed Chair reminds the markets that last Friday’s Jobs report was strong, but backward looking and lagging while other economic indicators show signs of s slowdown. The Fed does not want to over hike rates into a slowing economy and be the reason for the recession. So, while the market is currently pricing in two more rate hikes and a rate cut in December, this story could quickly change once again.

Bottom line:Rates and inflation have peaked. Housing activity has jumped in the past weeks as a result. The incoming data will determine how much better rates can get in the next few weeks leading to the next Fed Meeting.

Looking Ahead

Next week’s CPI is a very important number. If it meets or comes in lower than expectations, we could see home loan rates revisit the levels seen last week right before the Jobs Report last Friday. We will also see the latest readings on housing and the strength of the consumer, by way of Retail Sales. As fast as the story changed when the strong jobs data hit, things can change quickly upon these reports.

The all important CPI (consumer price index) inflation came out this morning and mixed news; the year over year January CPI report fell to 6.4%, which was a hair lower than last month’s 6.5% – which is good, but higher than market expectations of 6.2% – which could have been better.

Reminder inflation is the arch enemy of bond prices, and therefore mortgage rates, and the reason we’ve seen mortgage rates improve since what appears to have been the peak in November is because inflation has been coming down. CPI peaked last summer at 9.1%, and has since been steadily decreasing. It was the November & December CPI reports coming in lower than market expectations that were the impetus for mortgage rates improving over the past few months, and then last months data at 6.5% came in right at expectations, so today’s report was much anticipated and bucked the prior three month trend and came in higher than expectations.

Looking at the numbers from a month over month perspective, which is arguably the most relevant in measuring present trend, the month over month figure was up 0.5%, which was up from 0.1% last month. Shelter (housing) is the biggest factor here increasing 0.7%, making up the majority of the month over month numbers. National housing costs are not coming down.

This month’s jobs & CPI reports are now behind us, the labor marker remains very strong, and inflation is moving lower, albeit slowly. Inflation creeping lower is good, but as expected we should not expect a straight-line drop in prices, and there will be slower and outright pauses in declines going forward.

As a result of this morning’s CPI report, bond yields/mortgage rates have ticked a hair higher. See chart below of the 10 yr T, which jumbo rates are based on, for a graphical context. As you can see, rates peaked first week in November, have since come down a bit, and now giving up a bit of ground.

Regarding conversations with clients; 30 yr fixes in the 6%’s with option of getting into the 5% with points, is a healthy “normal” place for them to be, and still well below historical long term averages. We’re still seeing jumbo rates notably lower than conforming (approx ~.625% .75%). Lastly, even after rates have improved, considering grossing up a sale price & requesting a seller credit can still be a good strategy to get buyers into not just a more palatable rate, but one that is really quite good and a loan they may hold for as long as they’re in the property.

Interest rates hover near the best levels since September, despite several good economic readings reported. Let’s discuss what happened and see what is coming next week.

Gross Domestic Product, a measure of economic growth, for the Fourth Quarter 2022 showed the economy expanded at a 2.9% annual rate, down slightly from the 3.2% rate in the Third Quarter 2022. Seeing the economy grow in the back half of 2022 after negative growth in the first half of 2022 is good news.

This positive reading elevates the chance of a “soft landing” by the Fed, where they hike rates to slow inflation but do not slip us into a recession.

Unemployment Line is Historically Short

Initial Jobless Claims for December came in at 186,000…the lowest reading in 9 months. This is also good news as it tells us the length of the unemployment line. If the amount of people signing up for first time unemployment benefits remains near historical lows, it further lowers the chance of a recession. Moreover, it highlights the continued strength in the labor market, and this is paramount as jobs buy homes. Yes, we want interest rates to move lower but if someone doesn’t have a job or is in fear of losing their job, they can’t commit to a home purchase. Let’s hope the labor market remains strong as the Fed continues to hike rates to slow demand and lower inflation.

New Home Construction Costs Coming Down

The National Association of Homebuilders reported that building materials costs, less energy, are up 8.3% which is a big increase annually. However, the price growth is down a staggering 60% as input costs increased over 16% in 2021.

We should expect input cost growth to slow further in response to slower demand and further reopening of supply chains. This is another positive theme as we move through 2023.

Smaller Fed Rate Hike Still Priced In

One of the headwinds to the economy is the threat of higher short-term rates by the Federal Reserve. The good news there? After four consecutive .75% rate hikes, followed by a .50% hike in December, the financial markets are fully pricing in a smaller .25% hike at next week’s Fed Meeting.

The markets also believe the Fed will raise rates by another .25% in March and then pause to allow all the hikes that date back to last summer to seep into the economy.

This means the Terminal Rate, or the fancy way of saying the peak in the Fed Funds Rate, is going to be in a range of 4.75- 5.00%. From there we will have to continue to watch the standoff between the Fed who says they want to keep rates higher for longer. Additionally, with no rate cuts this year versus the financial markets, which are starting to “price in” as many as two rate cuts later this year.

Bottom line: The economy is showing mixed signals, but the labor market remains strong, and we are nearing the end of Fed rate hikes. So, the plan to land the U.S. economy softly and avoid a deep recession remains very much in play. That is good news for housing and the economy.

Looking Ahead

Next week is Fed week. As of this moment, the markets fully expect the Fed to raise rates by .25%. Anything other than that would be a surprise and generate a lot of market volatility. The Fed generally looks to avoid sending the market mixed signals but the markets will be on edge.

A federal emergency declaration has been proclaimed by President Biden and financial assistance may be forthcoming. While the federal government has not yet declared a disaster (a different designation that provides different resources) for California that could authorize direct financial assistance to affected residents.

Placer County requests those who have suffered damage to report itHERE.

If the issue is life threatening please dial 911. The intention of the survey is to allow the reporting of non-emergency issues during periods when the Emergency Operation Center is active. Your answers to the brief survey will help better document the extent of damage these storms have caused, so Placer County can continue to advocate for all available support for impacted residents.

With more weather still in the forecast, please use the Ready Placer Dashboard for the latest on road and weather hazards and to access resources to help protect your family and property.