We’re kicking off 2026 with a market that feels noticeably more active than a year ago. Across Lake Tahoe and Truckee, Q1 brought stronger momentum, with sales volume increasing across most segments and continued resilience in key areas of demand.

Lakefront properties once again led the way with sales volume doubling year over year, reinforcing just how limited and competitive this segment continues to be. We’re also seeing a clear geographic trend hold steady. Incline Village and Crystal Bay posted nearly a 50% increase in activity, reflecting continued buyer preference for Nevada-side inventory and its tax advantages.

Across the Tahoe Sierra MLS, overall sales volume rose about 7% year over year, while median pricing softened roughly 13%. This shift is less about declining values and more about a heavier concentration of sales in the mid and lower price points.

Luxury demand remains steady. Roughly 38% of all sales were above $2M, and 10% exceeded $5M—showing continued strength at the high end of the market even as it normalizes.

The standout remains the lakefront segment: not only did volume double, but pricing rose sharply year over year, with days on market down approximately 20%. Well-positioned properties continue to move quickly when they hit the market.

Overall, Q1 reflects a selective but healthy market with steady demand and clear opportunity as we move into the spring and summer season.

If you’re thinking about buying, selling, or simply want a real-time read on your property’s value, we’re always happy to connect.

Closing over $19M+ in Q1 is certainly worth celebrating. However, what matters most are the relationships behind the numbers.

This past quarter, in particular, was defined by repeat clients—many of whom we’ve had the privilege of working with since their first Tahoe investments in 2017. Because of that history, each transaction carries a deeper level of trust, understanding, and shared vision.

A Business Built on Trust & Longevity

Real estate is often measured in volume. Yet, for us, it’s measured in relationships.

Over time, those relationships evolve, from first purchases to portfolio growth, and eventually, to strategic sales. As a result, being part of these long-term journeys is not only meaningful, but it’s also the foundation of how we do business.

Repeat clients are the greatest reflection of trust. They return not just for results, but for guidance, consistency, and a thoughtful approach at every stage.

Welcoming New Clients Home to Tahoe

At the same time, this quarter also brought new opportunities to connect with clients discovering Lake Tahoe for the first time.

For those we had the honor of helping find home in this beautiful alpine community—welcome. We’re grateful to be part of your next chapter and to help you navigate what makes Tahoe living so special.

Looking Ahead to 2026

As we move further into 2026, the market continues to evolve. Therefore, whether you’re considering buying, selling, or simply planning what’s next, having the right strategy matters more than ever.

If a move is on your horizon this year, we’re here to guide you—every step of the way.

With Gratitude

Thank you to our clients for your continued trust and confidence. It truly means everything to us. We’re honored to be part of your Tahoe story.

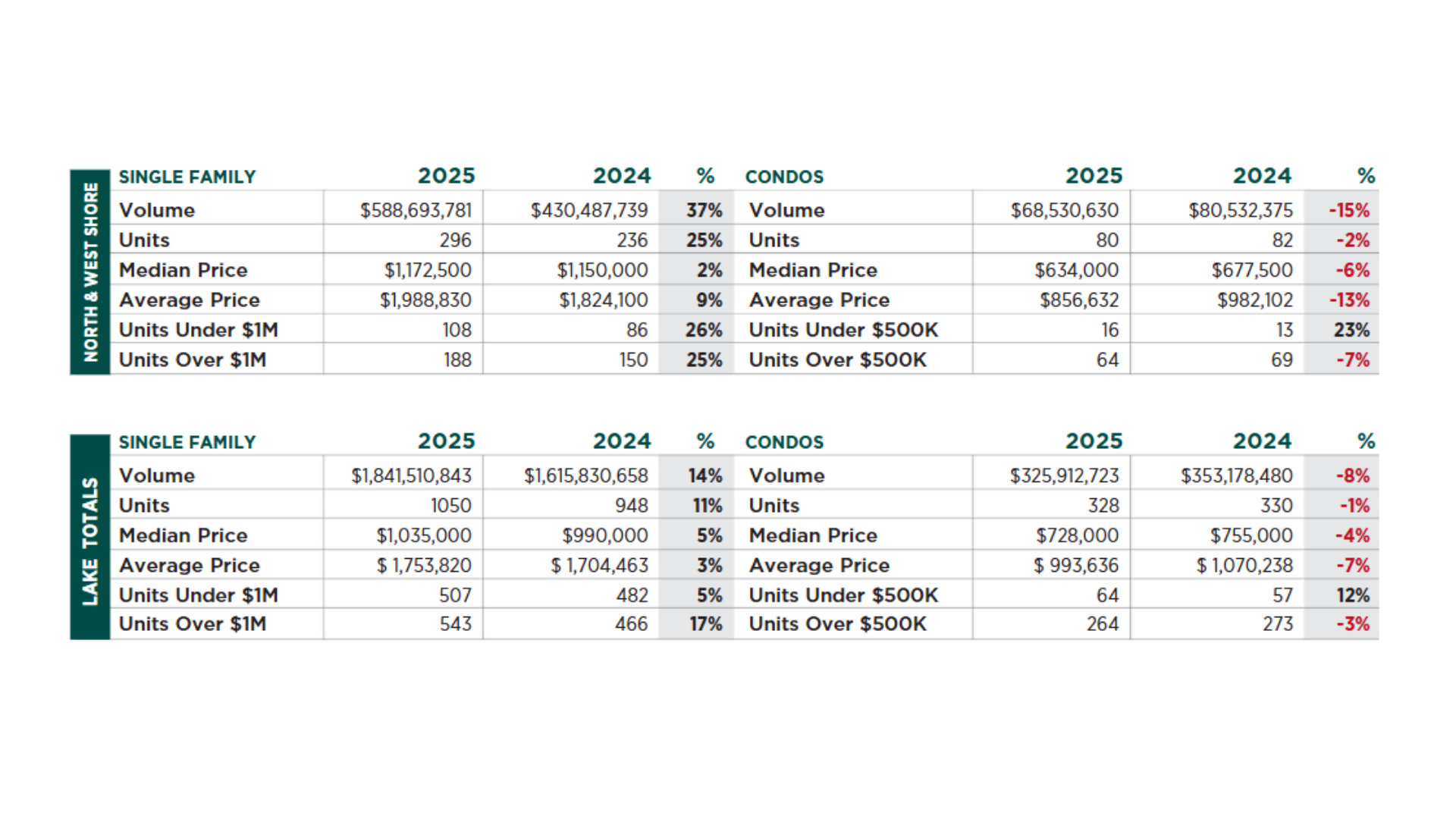

The Lake Tahoe real estate market moved through 2025 with steady momentum. Sales activity increased compared to the year before, while prices and days on market stayed relatively consistent. Overall, it was a market driven more by intention than urgency. Well-prepared and thoughtfully priced homes continued to attract strong interest.

Lakefront properties remained a standout, with renewed activity at the top of the market and strong demand from luxury buyers. Most lakefront sales closed above $5 million. On the North and West Shores, single-family homes also had a strong year, with increased activity, stable pricing, and more homes trading above $1M. Condo activity moved at a slower pace and was more selective, with buyers placing greater emphasis on space and long-term value.

The broader Tahoe picture is clear: buyers are engaged but selective. Success continues to come down to experience, presentation, and smart strategy. Our home selling strategies include a unique storytelling approach. We combine heavy digital and print media components, and connections that reach our primary feeder markets, as well as across the globe. If you are interested in learning the value of your home, we’d love to talk with you in an honest, no pressure way.

Incline Village home for sale at 541 Silvertip Drive

As we move into the fourth quarter of 2025, the Lake Tahoe real estate market continues to reflect thoughtful buyer decisions and strategic purchases. In Incline Village, total sales volume rose 26% year over year to $371.5M, marking a 15% increase in units. The average sale price climbed 10% to just over $3.2M, underscoring steady demand and the enduring appeal of Tahoe’s most desirable neighborhoods. Although the average days on market have risen by 52% year over year—showing a more deliberate pace among buyers—well-presented and well-priced properties continue to attract strong interest.

Compared to pre-pandemic levels, the market remains on solid ground. Since 2019, the average sale price has more than doubled, showing lasting appreciation rather than a short-term spike. Even with sales activity similar to 2019, today’s higher price points highlight a long-term shift in market values.

Throughout the third quarter, the market showed confidence and consistency. Buyers stayed active but selective, favoring move-in-ready homes in prime locations with standout design and outdoor spaces. Looking ahead to winter, the outlook remains positive—supported by Tahoe’s enduring appeal and reputation as one of the most desirable mountain destinations on the west coast.

Our home selling strategies include a unique storytelling approach, combined with heavy digital and print media components, and connections that reach our primary feeder markets, as well as across the globe. If you are interested in learning more about what the value of your home may be, we’d love to talk with you in an honest, no pressure way.

Steady Demand, Rising Values, and a Confident Winter Outlook

As we move into the fourth quarter of 2025, the Lake Tahoe real estate market continues to reflect thoughtful buyer decisions and strategic purchases. Both sales volume and median prices are up from last year, driven by steady demand and the limited availability of Tahoe’s most sought-after homes. Although the average days on market have risen by 52% year over year—showing a more deliberate pace among buyers—well-presented and well-priced properties are still drawing strong interest.

Compared to pre-pandemic levels, the market remains on solid ground. Since 2019, the average sale price has more than doubled, and the median price has climbed nearly 70%, showing lasting appreciation rather than a short-term spike. Even with sales activity similar to 2019, today’s higher price points highlight a long-term shift in market values.

Throughout the third quarter, the market showed confidence and consistency. Buyers stayed active but selective, favoring move-in-ready homes in prime locations with standout design and outdoor spaces. Looking ahead to winter, the outlook remains positive—supported by Tahoe’s enduring appeal and reputation as one of the most desirable mountain destinations on the west coast.

Our home selling strategies include a unique storytelling approach, combined with heavy digital and print media components, and connections that reach our primary feeder markets, as well as across the globe. If you are interested in learning more about what the value of your home may be, we’d love to talk with you in an honest, no pressure way.

Lake Tahoe Real Estate: Luxury Strength, Rising Inventory & Smart Opportunities

As we cross the halfway mark of 2025, the Lake Tahoe real estate market remains active and strategically balanced. While buyers have become more selective due to shifting interest rates and economic conditions, home values in many communities continue to rise, and inventory is returning to pre-COVID levels. Whether you’re considering buying or selling, now is a smart time to assess your position.

This update covers key insights across Incline Village, West Shore, North Shore, Tahoe Donner, and Truckee — with an eye toward helping you make informed decisions in today’s evolving market.

Key Mid-Year Trends

Inventory is up 19% YOY, with June 2025 inventory up 31%, nearing 2019 levels

Homes are selling faster, especially when priced and presented well

Pending sales are down ~40%, signaling buyer selectiveness, not weakness

Luxury demand remains strong, particularly near the lake

California-side median prices continue to rise, even with lower unit sales

Incline Village: High-End Still Holding Strong

Incline continues to shine as a destination for luxury buyers, fueled by Nevada’s tax advantages.

Mid-Year Snapshot – Incline Village

48 homes sold (↓ from 63 in mid-2024)

Median price: $2,056,875

Average price: $2,569,601

37 of 48 homes sold over $1M

✅ Turnkey, well-located homes are still commanding premium prices.

West Shore: Exceptional Value Growth

Even with fewer sales, West Shore values are soaring. This is a prime location for buyers seeking classic lakefront charm, privacy, and long-term equity.

Mid-Year Snapshot – West Shore

16 homes sold

Median price: $1,362,827 (↑19%)

Average price: $3,127,681 (↑97%)

9 of 16 sales over $1M

✅ Waterfront homes and secluded cabins continue to attract serious interest.

North Shore: Buyer Activity Rising

North Shore is heating up, with strong price gains and rising buyer activity. Accessibility to beaches, ski resorts, and walkable towns makes this a versatile option for full-time and part-time owners.

Mid-Year Snapshot – North Shore

18 homes sold (↑ from 15 in mid-2024)

Median price: $1,397,500 (↑27%)

Average price: $2,034,166 (↑73%)

14 of 18 sales over $1M

✅ Buyers continue to value lifestyle, location, and long-term potential.

Tahoe Donner: Active & Affordable

Tahoe Donner remains a top choice for buyers seeking value, amenities, and rental flexibility. This market supports both primary homeownership and second-home investments.

Mid-Year Snapshot – Tahoe Donner

33 homes sold

Median price: $1,060,000

Average price: $1,091,015

✅ Inventory is healthy, and well-prepped homes are moving.

Truckee: High Volume, High Demand

Truckee leads the region in total sales. From resort neighborhoods to family-friendly communities, the market here appeals to a wide range of buyers — especially Bay Area relocators.

Mid-Year Snapshot – Truckee

93 homes sold

Median price: $1,299,000

Average price: $1,661,939

✅ Truckee offers lifestyle, infrastructure, and community in one package.

What’s in It for Buyers Right Now?

Even in a strong market, buyers have unique advantages today:

More inventory = more choice. June saw the biggest YOY jump in available homes since pre-pandemic.

Negotiation power is increasing. With pending sales down 40%, selective buyers can act strategically.

Days on market are shortening, but turnkey properties still offer room to move fast and negotiate.

Tax-friendly zones like Incline Village appeal to those looking to optimize long-term value.

Why Late Summer Matters

Late summer into early fall is one of the busiest windows for real estate activity in Tahoe. Whether you’re planning to buy or sell, this is when:

Buyers look to purchase before winter

Investors and cash clients are most active

Sellers can maximize seasonal visibility

Let’s Talk Strategy — For Sellers or Buyers

If you’re considering selling, buying, or both, this market offers rare clarity and strategic timing. The Chase International market reports offer the insights you need to stay ahead, and I’m happy to walk you through the trends and tailor a plan based on your goals. Read the full 2025 Mid Year Update here

? Request a private home valuation or buyer consultation today. I’m here to help you move confidently — and smartly — in 2025.

Lake Tahoe Real Estate: A Steady Favorite in an Unsteady World

Navigating through tariffs, stock market fluctuations, and our ever-changing world, one thing remains constant: people love Lake Tahoe. It is as beautiful as it is simple — and that’s why we continue to believe in the lasting strength of our local real estate market.

The Chase International 2025 Q1 Market Reports are in, and they offer a revealing snapshot of buyer behavior and property performance across the Lake Tahoe basin. Here’s a look at what’s happening in Incline Village, the West Shore, and the North Shore.

Incline Village: Luxury Still Leads

In Q1 2025, Incline Village saw 19 units sold — a significant drop from 30 in Q1 2024, yet the market’s luxury strength remains notable.

Median Price: $1,850,000

Average Price: $1,959,842

Homes Over $1M: 15

Homes Under $1M: 4

Despite a -37% decline in units sold, the market held strong with luxury demand. Median prices were down slightly from last year, but with 100% more homes sold under $1M (4 this year vs. 2 in 2024), there’s a signal that opportunity exists at every level of the market.

West Shore: A Rise in Value

The West Shore had 16 units sold in Q1 2025. While this reflects a small decline from last year (19 units in Q1 2024), property values are rising fast.

Median Price: $1,362,827 (+19%)

Average Price: $3,127,681 (+97%)

Luxury homes dominated the market with 9 of the 16 sales over $1M, indicating a strong preference for waterfront and exclusive West Shore living. This area is clearly gaining traction as a premium destination within Tahoe.

North Shore: Momentum Building

The North Shore showed encouraging signs with 18 units sold, up from 15 in Q1 2024 (+20%).

Median Price: $1,397,500 (+27%)

Average Price: $2,034,166 (+73%)

Homes Over $1M: 14

Homes Under $1M: 4

The North Shore’s appeal continues to grow, especially among luxury buyers. With a jump in both median and average price, this area reflects a market that’s not just holding steady — it’s accelerating.

Why It Matters

Across all three areas, one theme is clear: buyers continue to choose Lake Tahoe for its beauty, lifestyle, and investment potential. While unit volume may fluctuate with broader economic forces, home values and high-end interest remain strong.

Q1 2025 Sales Snapshot (All Areas):

✅ Incline Village: 19 units sold ✅ North Shore: 18 units sold ✅ West Shore: 16 units sold ✅ Truckee: 93 units sold ✅ Tahoe Donner: 33 units sold

Whether you’re a potential buyer, seller, or investor, the Chase International market reports offer the insights you need to stay ahead. Read the full Q1 2025 Market Stats here.

? Want a personalized market breakdown or a valuation of your home? ? Click here or DM me anytime.

Stay informed. Stay confident. — Amie with The Q Group

Lake Tahoe continues to be a premier luxury destination and a strong investment market, attracting buyers seeking second homes, vacation retreats, and high-value real estate opportunities. Known for its stunning natural beauty, world-class outdoor recreation, and desirable year-round lifestyle, the region remains a hot spot for both primary and secondary homeowners.

As we move into 2025, the Lake Tahoe home market remains highly competitive, with low housing inventory driving demand, particularly in sought-after areas such as lakefront properties, ski-in/ski-out homes, and luxury mountain estates. Buyers looking in the neighborhoods of the West Shore, North Lake Tahoe, Tahoe City, and Incline Village will continue to face a fast-moving market, as limited supply and high desirability keep home prices strong.

For potential buyers, understanding Lake Tahoe market trends, median home prices, and luxury real estate appreciation is essential for making smart investment decisions. Market conditions, including interest rates, seasonal fluctuations, and buyer demand, will shape opportunities throughout 2025, influencing affordability and competition. Those interested in purchasing a home should work with a local expert to navigate pricing trends, negotiate effectively, and identify the best properties before they hit the broader market.

Sellers also stand to benefit from the ongoing demand, as well-maintained and well-located properties continue to attract interest from buyers looking for Lake Tahoe vacation homes, investment properties, and full-time residences. Proper pricing and expert guidance will be key to maximizing returns in this dynamic market.

Whether you’re considering purchasing a Lake Tahoe luxury home or listing your property for sale, staying ahead of real estate trends is crucial. Thinking about buying or selling in Lake Tahoe in 2025? Contact The Q Group today for expert insights, exclusive listings, and personalized real estate guidance tailored to your needs.

As a luxury destination and strong investment market, Lake Tahoe’s appeal remains robust. For 2025, low inventory is expected to drive competition and sustain strong pricing, particularly in high-demand segments like lakefront and luxury properties.

The Lake Tahoe real estate market remains dynamic as we close out the year. Here’s a snapshot of current market conditions across key areas:

These numbers reflect a mix of opportunities and challenges for buyers and sellers. If you’re considering entering the market, now is a great time to discuss your goals with a real estate professional who understands Tahoe’s unique market.

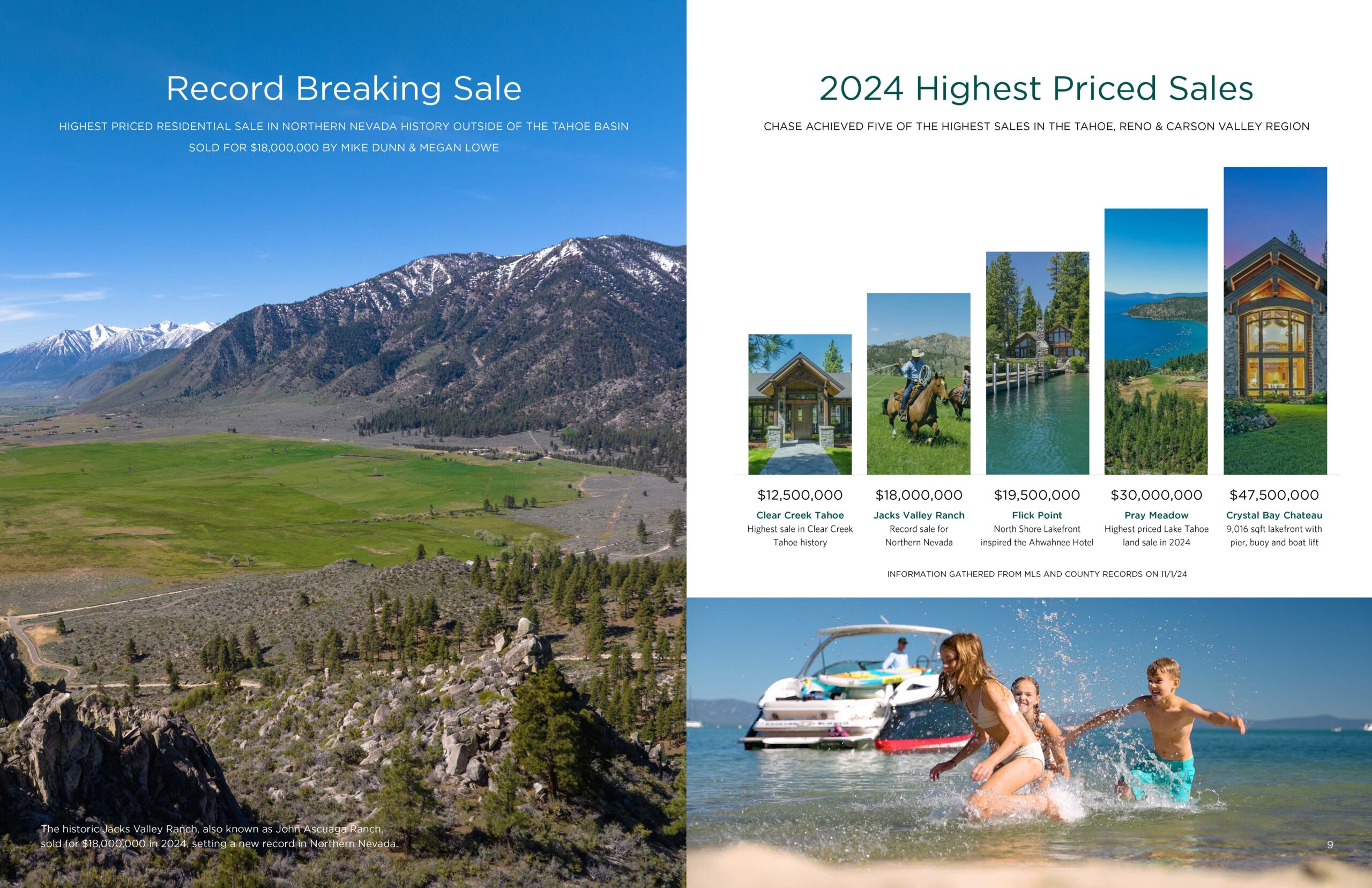

The Lake Tahoe luxury market experienced significant growth in 2024, highlighted by record-breaking sales and strong demand. A landmark transaction set a new benchmark for the Tahoe Basin, reflecting the appeal of the region’s high-end properties. While some areas saw substantial increases in activity, others faced slight declines, all underscored by a persistent inventory shortage driving prices upward. Despite these challenges, property values remain stable, supported by sustained buyer interest.

For more information on Lake Tahoe properties or questions on the real estate market, contact Amie Quirarte with The Q Group.